Retail on the Rise: Australia’s shopping centre revival

An omni-channel retail evolution

Not long ago, shopping centres across Australia were under significant pressure, with convenience-type centres appearing more resilient. Hammered by e-commerce, pandemic restrictions and changing consumer habits, the demand for retail floorspace (how much and where) was the perennial question.

Fast-forward to today and the story is shifting. Shopping centres under threat have reinvented themselves. They have emerged stronger by embracing roles as vital nodes in omni-channel retail and as local community hubs. But to remain relevant, shopping centres must continuously adapt in response to changing consumer demands.

Here we consider what has happened, how things will evolve, and why local governments are so important.

From Zero to Hero: Retail has emerged from the wilderness

For a decade or more, retail has been under substantial pressure. Growing e-commerce and evolving consumer tastes which preferenced spending on experience over owning physical goods, together with forced pandemic-related closures, upended traditional business models. Retail insolvencies spiked. Australia was left with too much unneeded retail floorspace, ill-adapted to structural change. Vacancy spiralled and investment plummeted in many retail centres across the country.

Today though, shopping centres have staged a comeback. Owners have reinvested in their assets to reposition and reinvigorate their offer. Place-made amenity space like dining concessions (such as Foodle at Highpoint in Melbourne), wellness uses and kids’ activity zones are in demand. Whereas, fashion, household goods and department store space has shrunk. There is now a revolving roster of pop-up retailers and entertainment to keep the offer fresh and exciting for customers.

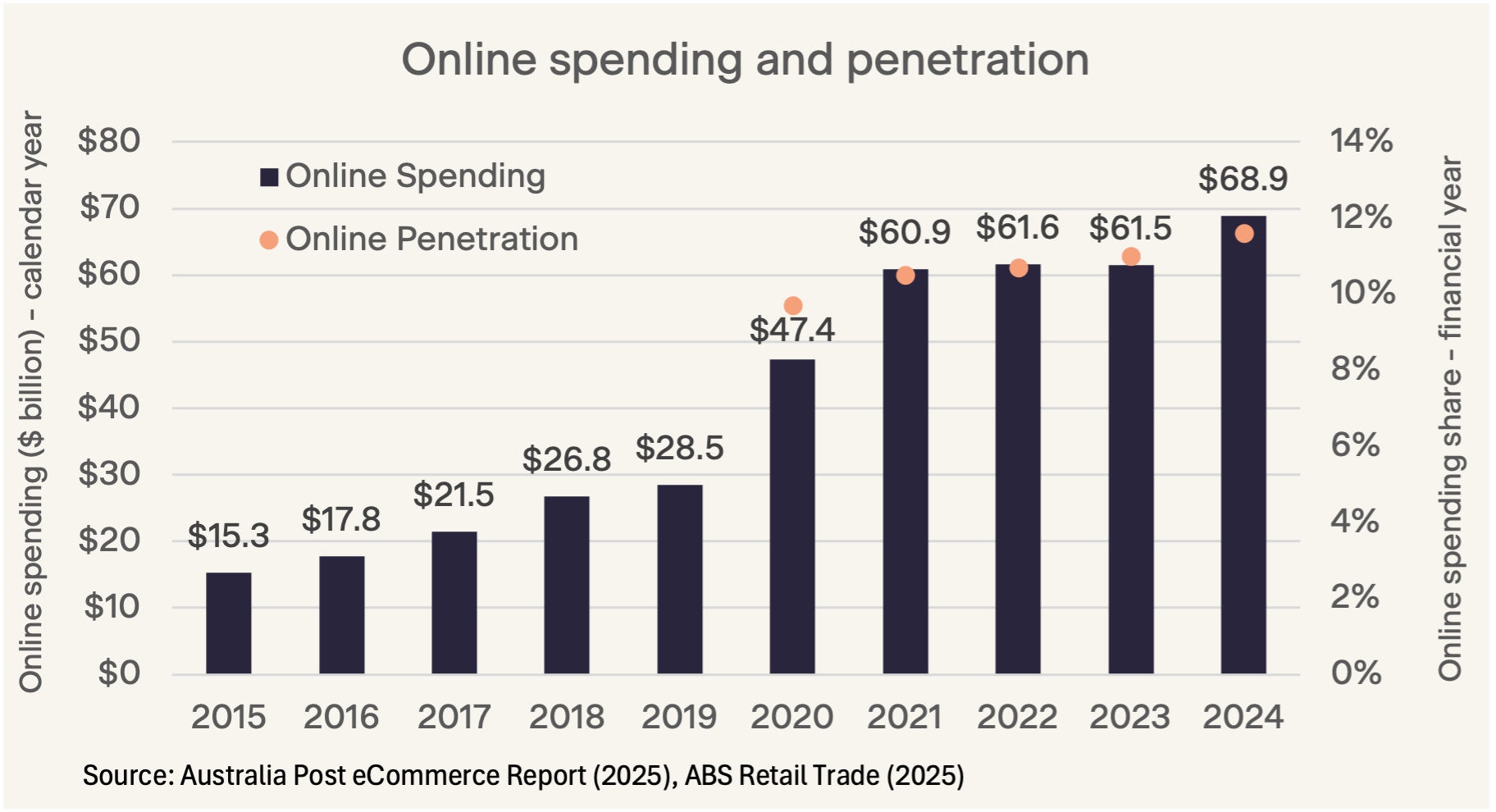

Aiding the revival, e-commerce penetration appears to be plateauing1. Online penetration reached nearly 13% in June, but the rate of growth is slowing. Australia may end up mirroring the US where e-commerce tapped out around 16%3.

In any case, shopping centres have leaned into an omni-channel model. One where they benefit either way through initiatives like ‘click & collect’ and/or delivery from their bricks and mortar stores. It's estimated that 91% of future Australian sales growth over the next decade is predicted to involve a physical store4. Meaning the need and enthusiasm for shopping centres will be undiminished.

Figure 1: Online Spending

An Evolving Mix: Change is the only constant

Retail’s improving fortunes have encouraged investors back into the market. Investment volumes grew by 40% in Q2 2025 compared to Q1 and shopping centre yields compressed5. Increasing deal activity in the future is likely. As demand grows, supply is tight. Despite population, employment and ongoing retail expenditure growth, no new regional centres are on the horizon. Due mainly to high construction costs and the challenges with securing sites and planning support6. This will encourage centre owners to carry on investing in their existing assets to maximise their economic value. Creating features such as centre ambience upgrades, placemaking design, and community engagement.

We also expect shopping centres to evolve beyond pure retail and leisure. Complementary uses like housing and flexible working suites will be layered on top of centres. Examples of this includes The Glen and Chadstone in Melbourne. Such diversification raises new revenue streams for owners, bringing additional spend for occupiers. As well as much needed housing and workspace for the public. It also accords with sustainability principles by concentrating new development on existing well-serviced and accessible urban land.

Repurposing: Excess floorspace has opened other opportunities

The struggles of department stores have been well documented over the last decade. David Jones, Myer, Big W and Target have all given back space and reduced the number of stores they operate. This has provided retail landlords with a major opportunity to attract a different customer segment to their assets. Key case studies include:

- Westfield Knox (Melbourne): Myer was partially replaced with a library, basketball court and swim school in 2023

- Indooroopilly Shopping Centre (Brisbane): A car dealership was added to level 3 of the regional shopping centre in 2022

- Imperial Centre Gosford (Central Coast): ET Secondary College opened in 2021 on the second level of the neighbourhood shopping centre

- Carrum Downs Regional Shopping Centre (Melbourne): Woolworths began filling online orders out of excess space at the shopping centre in 2020

Some of the excess floorspace once devoted to clothing and apparel is now being reconfigured for non-retail uses. This includes community, education, eCommerce and even automotive based tenants. Strength lies in the ability to quickly repurpose space within a shopping centre to an alternative use.

Adaptability: Planning has a crucial enabling role

Australia’s shopping centres have weathered the storm of e-commerce, fickle consumers and COVID-19, and emerged stronger. They have proven themselves as local community anchors meeting vital economic and social needs. Their importance will grow over time.

However, to remain relevant they must also continue to adapt. There are multiple recent examples of centres evolving. From Scentre Group’s plans to expand and include 1,500 apartments at Warringah Mall in Sydney’s Northern Beaches, to Holdmark’s plan to add up to 500 homes at Caddens Corner, NSW. In Melbourne, examples include plans for residential towers at Box Hill Central and the Jam Factory in South Yarra.

In this context of ongoing centre evolution, local planning authorities have a crucial role in enabling their success. Frequent design and land use tweaks are necessary to align with shifting consumer tastes. As their land use mix broadens, planning flexibility is necessary. By adopting a supportive attitude and a partnership approach with shopping centre owners, local governments can maximise the potential of the shopping centre revival for the benefit of their communities.

References

1 Australia Post (2025). eCommerce Report 2025. Australia Post. Available from: https://auspost-report.s3.ap-southeast-2.amazonaws.com/AUS+Post+-Ecommerce+Report+2025.pdf

2 ABS (June 2025). Retail Trade, Australia. Available from: Retail Trade, Australia, June 2025 | Australian Bureau of Statistics

3 Quay Global Investors (August 2025). Investment Perspectives: 10 charts shaping our thinking. Available from: Investment Perspectives: 10 charts shaping our thinking | Quay Global Investors - A Bennelong boutique

4 GPT (2025). Retail Recharged: A look through the investment lens. Available from: https://www.gpt.com.au/news-insights/retail-recharged-look-through-investment-lens

5 CBRE (Q2 2025). Shopping centre yields compress amid improving sentiment and sales. Available from: Australian Retail Figures Q2 2025

6 Colliers (Q2 2025). Australian Retail Snapshot. Available from: colliers-autralian-retail-snapshot-q2-2025.ashx

Related posts

Dive deeper into insights that matter to you.

Atlas Economics is now a proud and excited partner of the Goodes O’Loughlin (GO) Foundation!

Atlas Housing Download Series: Part 3 - Regulatory Change in Building Requirements and Cost Implications

Atlas Housing Download Series: Part 2 - Capacity and Capability of the Construction Sector in Australia

Atlas Housing Download Series: Part 1 - Population Growth and Dwelling Production

Make smarter decisions

Get in touch with the Team to get an understanding of how we transform data into insightful decisions. Learn more about how Atlas Economics can help you make the right decisions and create impact using our expertise.